There is general agreement that the banking sector should pay for its own safety net, meaning that resolution and deposit guarantee funds should be financed by contributions from the banks themselves. This principle lies at the heart of the approach taken in the EU Directive on (national) Deposit Guarantee Schemes (DGS) and is enshrined in the basic rules of the Single Resolution Fund (SRF). Moreover, there is also a consensus that contributions should be based on the risk profile of each bank – as an essential precondition to providing individual banks with the proper incentives to internalise the potential costs related to bank failure. It is, however, questionable whether the current methodology to calibrate contributions fully succeeds in this aim.

The SRF was established in 2016 in the context of the Single Resolution Mechanism (SRM). The main aim of the SRM is to resolve banks in an orderly manner without public funds. However, since it is unlikely that all financing in resolution can be arranged via bail-ins and monetary facilities, additional funds for resolution might be required. The role of the SRF is to provide these funds.

The overall target size of the SRF has been determined as 1% of covered deposits (approximately €60 billion).

The contribution expected from each bank each year during the build-up phase is not just proportional to the covered deposits at that bank, but depends instead on a large number or risk indicators. In principle, it makes sense to relate contributions to risk. But the way this is done raises some issues.

First, the risk indicators should not just reflect the likelihood that a bank might fail, but rather that the failure of a bank will require an intervention by the SRM leading to losses for the SRF. The ‘loss-making’ qualification is important in this context because the SRM is supposed to provide funding only when an appropriate use of bail-in tools has re-established a solvent entity. It is of course possible that, ex post, an intervention of the SRF leads to losses, but ex ante, this is not a foregone conclusion. Funding a resolution after bail-in should thus be viewed as an investment, rather than an automatic loss. Any investment brings risks, but also a potential upside. This distinguishes resolution funds from deposit insurance funds. The latter only intervene to protect covered deposits, so any intervention by a deposit insurance fund thus signifies a loss.[1] This difference in the nature of the intervention implies that one should apply different risk criteria for the contributions to a deposit insurance fund and contributions to a resolution fund, such as the SRF.

A second fundamental issue is that contributions to the SRF will stop once it has reached its target size. But this implies that after that date, the incentive effect of contributions related to risk parameters will no longer operate. This second issue is a relatively straightforward corollary, but the first one, identifying risks for the SRF, requires more thorough analysis.

Current methodology for setting annual contributions

At present, the contribution of each bank to the build-up of the SRF is determined in a two-step procedure.

In a first step, the annual contribution expected from the entire banking system to the SRF is calculated so as to reach the 1% target by 2024. In a second step, this overall amount is distributed across individual banks according to a combination of size, business model and risk characteristics.

Small institutions with total assets of less than €1 billion pay a lump sum contribution. This contribution varies between €1,000 and €50,000 depending on the contribution base, i.e. total liabilities minus own funds and covered deposits. In 2018, this category formed the largest group: 49% of the 3,315 contributing institutions.

Mid-sized institutions with total assets between €1 and €3 billion pay a combination of a lump sum contribution and a risk adjusted contribution. The lump sum is paid over the first €300 million contribution base, which is identical to the maximum contribution base for small institutions. The risk-based contribution is calibrated over the remaining contribution base. In 2018, this category formed the second largest group: 28% of the 3,315 contributing institutions.

Large institutions with total assets above €3 billion pay a fully risk adjusted contribution. In 2018, this category formed the smallest group: 21% of the 3,315 contributing institutions. However, they are responsible for 96% of the total contributions to the fund.

Non-bank institutions are subject to a specific calibration of contributions. Covered bond financed mortgage credit institutions and investment firms form only a small share of the institutions subject to contributions.

The delegated regulation that determines the risk adjusted contribution of each bank to the SRF is based on a number of elements or ‘pillars’. The most obvious ones are risk and liquidity factors. Two additional ones are interconnectedness and ‘additional risk indicators’. Article 7 of the relevant delegated regulation also gives the weights for each factor.

When assessing the risk profile of each institution, the resolution authority is instructed to apply the following weights to the risk pillars:

- Risk exposure (50%);

- Stability and variety of sources of funding (20%);

- Importance of an institution to the stability of the financial system or economy (10%);

- Additional risk indicators to be determined by the resolution authority (20%).

The precise elements constituting each pillar are then further defined in terms of specific balance sheet and regulatory indicators. However, due to the unavailability of harmonised data, the SRB has removed several indicators from the methodology, leaving the set of indicators and risk-weights for the calculation of contributions in 2018 as presented in Table 1 above.

Risk for the SRF

The basic approach followed so far to determine the contributions banks have to pay to the SRF is thus based on a number of different balance sheet and regulatory indicators, mostly using ratios, which constitute key elements of prudential rules. At first sight, this seems reasonable. However, it is not clear why these factors would adequately represent the risk for the SRF.

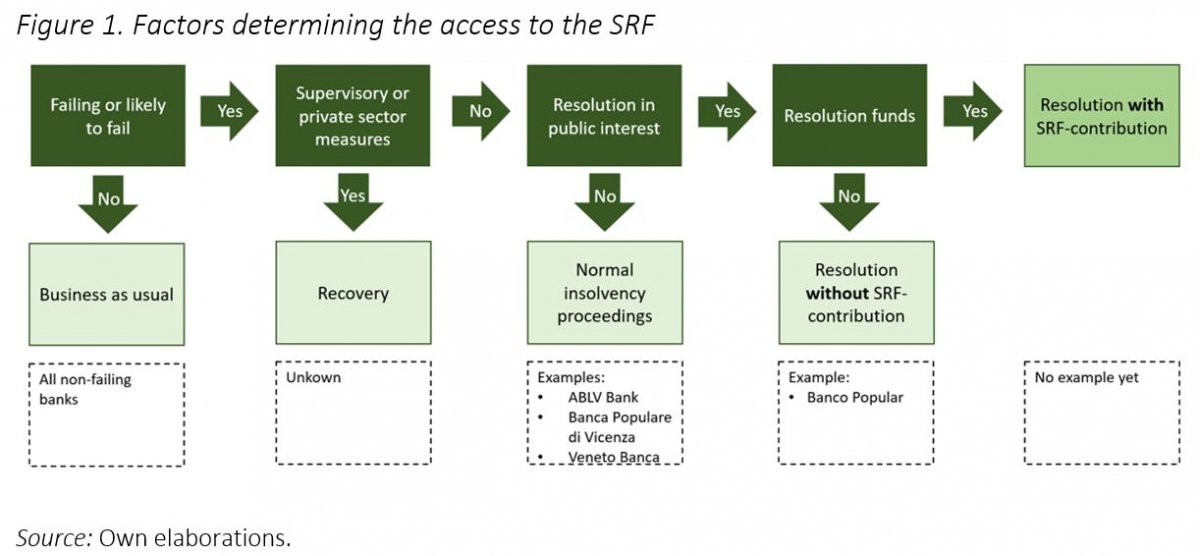

The granting of support by the SRF is far from automatic for failing banks, as the first failures since the establishment of the fund have shown. Indeed, the resolution mechanism aims to address bank failures with private solutions or the normal insolvency proceedings (Figure 1). The bank will only be resolved when these are deemed inappropriate and there is a public interest.

When the SRF is used, it can be used for various purposes including providing guarantees, loans, purchasing assets, and compensating creditors that are worse off than under normal insolvency procedures. However, the fund has been primarily designed for recapitalisations that are conditional on a minimum bail-in of liabilities (König, 2018).

The current methodology does not adequately capture these factors, which are those that determine whether a bank constitutes a risk for the SRF. It focuses primarily on the likelihood a bank may fail and much less on the chance of a resolution and the potential involvement of the SRF. For example, the covered deposits that are one of the main elements in the public interest assessment are exempted from the contribution base, whereas instruments that can be bailed in (and therefore likely to bear losses in a resolution) form a significant part of the base for the calibration. This means that some banks are currently paying relatively too much and others too little.

The potential risks for the SRF can be estimated. For example, we calculated in 2015 the total losses that would have been incurred by EU banks if all banks in receipt of capital support in the aftermath of the financial crisis had been resolved. We found that the funds required from the SRF would have been limited. The headline finding of that study was that the total losses incurred by the banks needing support amounted to about €313 billion. This figure looms large relative to the present and future size of the SRF. But the same figure also appears small relative to the total balance sheet of these banks – less than 3% of total assets. There are two key explanations for the relatively low contribution: the SRF can only intervene after a bail-in of a minimum 8% of liabilities including own funds, while the funding from the SRF is limited to 5%.

Figure 2 below shows a scatter plot with the losses on the horizontal and the hypothetical contribution of the SRF on the vertical axis. A best fit line can explain only about one half of the variability in the SRF contribution and the four big cases in the oval on the right illustrate that for losses around €25 billion, the contribution of the SRF could have been either zero (Fortis, with a low risk-weighted assets/total assets ratio) or €15 billion (Bankia). Moreover, almost all cases lie below 50%, meaning that in only a very few cases would the SRF have covered more than one half of the losses.

Making the contribution to the SRF really risk-based

These results suggest that expected losses do not translate directly into a risk for the SRF. What is needed is an analysis of which characteristics of a bank imply a risk for the SRF, thus justifying a modification of the methodology.

Over the next few months, CEPS will conduct an exercise to come up with a methodology for the annual contributions for the SRF that reflects the risks to the SRF more closely. For this we will estimate the risk adjustment factor, contribution base and contribution to the SRF for individual banks and banking groups. Moreover, we will, based on the information available on the resolution mechanism, design a methodology that is risk-based and assess how this would affect the 3,315 institutions that contribute to the SRF. The results of this exercise are expected in the spring of 2019.

References

De Groen, W P and D Gros (2015), “Estimating the Bridge Financing Needs of the Single Resolution Fund: How expensive is it to resolve a bank?”, CEPS Special Report No. 122, CEPS, Brussels, November.

European Commission (2014) COMMISSION DELEGATED REGULATION (EU) 2015/63 of 21 October 2014 supplementing Directive 2014/59/EU of the European Parliament and of the Council with regard to ex ante contributions to resolution financing arrangements.

König, E. (2018). “Gaps in the Banking Union regarding funding in resolution and how to close them”, Eurofi, Article (https://srb.europa.eu/en/node/621).

Daniel Gros is Director and Willem Pieter de Groen is Research Fellow and Head of the Financial Markets and Institutions Unit at CEPS.

CEPS Commentaries offer concise, policy-oriented insights into topical issues in European affairs. As an institution, CEPS takes no official position on questions of EU policy. The views expressed are attributable only to the authors and not to any institution with which they are associated. CEPS gratefully acknowledges the sponsorship received for this research project from Fédération Française Bancaire (FBF).

© CEPS 2018?

[1] If a bank is liquidated, the deposit insurance fund pays out for the covered deposits and receives in exchange a claim on the bank in liquidation. The maximum a deposit insurance fund can recover is the amount of deposits it compensated and it will thus never make a profit on its interventions.